If you’ve been involved in a car accident and are seeking compensation, it may be likely that you have to pay a deductible. Some victims of car accidents assume that if they were not at fault in their accident, they would not have to pay their deductible. However, this is normally not the case. In the State of Florida, you have to pay your deductible even if the accident was not your fault. Having said this, if another party is proven to be at fault in your accident, you may have the opportunity to claim compensation to recover the deductible from your insurance company.

Recovering from the mental and physical damages after a car accident is often a long and grueling process, especially when financial burdens of medical costs and other expenses are involved. These damages are significantly more worrisome when you include the total amount of the deductible that must be paid to the insurance company.

If you have been involved in a car crash in Florida, call The Law Place today. Our attorneys have over 75 years combined experience across multiple practice areas, including personal injury law, and know how to get the compensation that you deserve for your accident. With the help of an experienced legal team, you can rest assured that your case is in capable hands while you recover from the accident.

You can contact The Law Place by phone or by visiting us at our law office. Our phone lines are always open so feel free to contact us whenever it suits your schedule best. Call us today at (941) 444-4444 and schedule your free consultation with one of our top personal injury attorneys to discuss your insurance policy, coverage, and deductible.

What Is a Deductible?

When entering into a contract of insurance coverage for your vehicle, clients often have a deductible payment that they agree to. If you have been involved in an accident and want to file a claim with your insurance company, you will be obliged to pay this amount before the insurance company covers the rest of the damages. For example, if your deductible is $300 and the medical care you received as a result of your accident costs $1,000, you will pay the $300 deductible, and the insurance provider should cover the remaining cost of $700.

In Florida, car insurance deductibles typically range between $250 to $1,000. People that pay a premium price for their insurance coverage will often have smaller deductibles. In other words, if you have a lower insurance premium, your deductible will be considerably higher. In some cases, an insurance company may offer a $0 deductible in their insurance policy if the client’s insurance premium is particularly high.

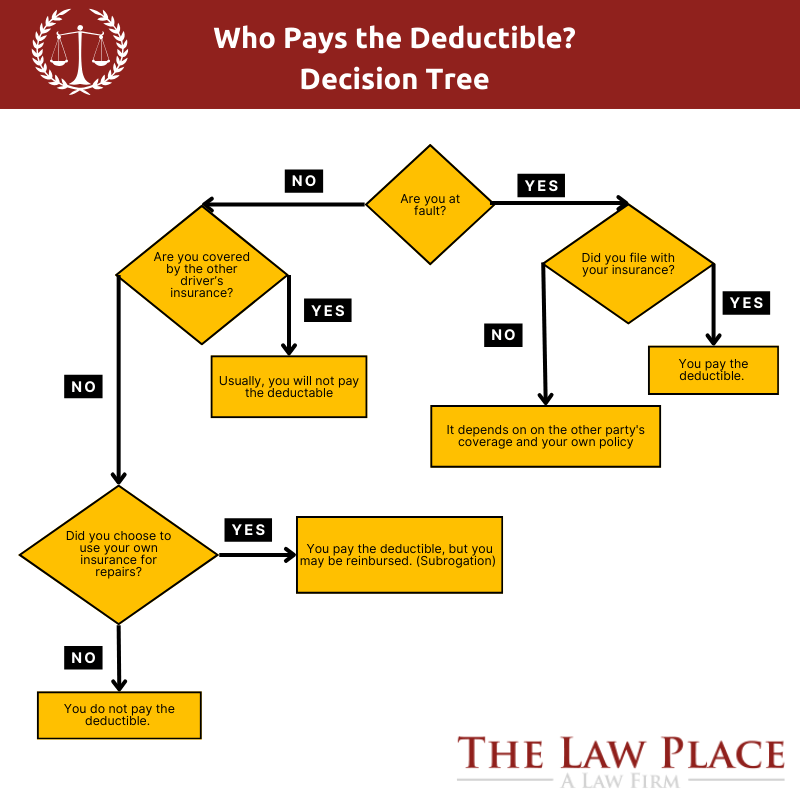

Who Pays the Deductible? Decision Tree

Do You Get Your Deductible Back If You’re Not at Fault?

A common question among those involved in car accidents where they are not at fault is whether they can recover their insurance deductible. Understanding how this process works can provide clarity and help in managing post-accident financial concerns.

If you are involved in a car accident and are not at fault, it is possible to get your deductible back. This typically happens in one of two ways:

Through Subrogation

The most common way to get your deductible back is through a process called subrogation. In this process, after you file a claim with your own insurance company and pay your deductible, your insurer will seek reimbursement from the at-fault party’s insurance company. If your insurer is successful in proving the other driver’s fault and recovers the costs, you will typically be refunded your deductible. This process can take time, depending on the complexity of the case and the efficiency of the insurance companies involved.

Subrogation Process

Subrogation is the process by which your insurance company seeks to recover the amount it paid for your claim, including your deductible, from the at-fault driver’s insurance company. Here’s how it works:

- Your Insurance Pays for Repairs: After an accident, you can choose to file a claim with your insurance company and pay your deductible. Your insurance will cover the remaining repair costs.

- Investigation and Determination of Fault: Your insurance company will investigate the accident and determine who was at fault.

- Seeking Reimbursement: If the other driver is found to be at fault, your insurer will seek to recover the costs, including your deductible, from the at-fault driver’s insurance company.

- Reimbursement to You: Once the subrogation process is complete, and your insurance company has been reimbursed, you will get your deductible back. This process can take several weeks to months, depending on the cooperation between the insurance companies and the complexity of the case.

Direct Reimbursement from the At-Fault Driver’s Insurance

Alternatively, if you can clearly establish the other driver’s fault, you can file a claim directly with the at-fault driver’s insurance company. If the claim is accepted, you would receive compensation for the damages, including your deductible, without having to go through your own insurance. However, this approach might involve more direct negotiation and communication with the other party’s insurer and can be more time-consuming.

It’s important to note that the ability to recover your deductible largely depends on the clarity of fault in the accident. If fault is disputed or if you are in a state with comparative negligence laws, where fault is shared, recovering your deductible might be more complicated.

In scenarios where fault is not immediately clear, or insurance companies are in the process of negotiating, you might have to initially bear the burden of the deductible. However, once fault is established and if it lies with the other driver, you should be able to recover this amount.

We’re here to serve you. Our phones are open 24 hours a day.

We’re here to serve you. Our phones are open 24 hours a day.

Impact of Different Coverage Types

Different types of car insurance coverage involve different deductible scenarios. Here’s a breakdown:

- Collision Coverage – Pays for repairs to your vehicle after an accident, regardless of fault. You must pay your deductible before your insurance covers the remaining repair costs.

- Comprehensive Coverage – Covers damage to your vehicle from non-collision events like theft, vandalism, or natural disasters. A deductible applies in these cases as well.

- Uninsured and Underinsured Motorist Coverage – If the at-fault driver is uninsured or underinsured, this coverage can help pay for your damages. Deductibles may apply depending on your policy.

- Liability Coverage – This is required by law in most states and covers damages you cause to others. It typically does not have a deductible.

We’re Florida’s top litigation team with over 75 years of combined experience

We’re Florida’s top litigation team with over 75 years of combined experience

Steps to Take After an Accident

After an accident, taking the right steps can help ensure a smoother claims process:

- Stay at the Scene – Remain at the scene of the accident and ensure everyone’s safety. Call the police to file a police report, which will be essential for your insurance claim and any potential legal proceedings.

- Collect Information – Exchange information with the other driver(s), including names, contact details, insurance information, and vehicle details. Gather witness statements if possible to support your case.

- Document the Scene – Take photos of the accident scene, vehicle damage, and any injuries. These can be crucial for both your insurance claim and any legal case.

- Contact Your Insurance Company – Report the accident to your insurance company as soon as possible. Provide them with all the necessary information and documentation, including the police report.

- Seek Medical Attention – Even if you don’t feel injured, it’s essential to get a medical check-up to ensure there are no hidden injuries that could affect you later.

- Contact The Law Place – Reach out to The Law Place to discuss your case with an experienced car accident attorney. Our team can guide you through the legal process, protect your rights, and help maximize any compensation you may be entitled to. Call us at (941) 444-4444 for a free consultation.

From the initial call to updates on your case status, we are here to get you answers.

From the initial call to updates on your case status, we are here to get you answers.

Do I Have to Pay the Car Insurance Deductible if I Didn’t Cause the Accident?

If you have suffered damages from your accident, including vehicle damage, and want to claim compensation from your insurance company to cover these costs quickly, you will have to pay the deductible. Your insurance company, as well as the other driver’s insurance company, will review your claim in order to determine who was liable for the accident and calculate how much compensation you may be entitled to, which can take months or maybe years to be agreed upon and finalized.

If it is determined that you were not at fault for the accident, your insurance company may be able to claim damages from the at-fault driver’s insurance provider for the collision. This can often cover the cost of the car insurance deductible as well as other damages incurred due to the crash.

With the expertise and support of experienced legal representation at The Law Place, you may be able to claim compensation without having to rely on your insurance provider. Our personal injury attorneys can determine liability in a car accident case and calculate how much you may be owed in compensation. Seeking compensation with the help of our attorneys can help cover the costs of the deductible amount as well as other damages incurred, including lost wages and medical expenses.

Florida’s No-Fault Insurance Laws

As per Florida Statute 627.7407, Florida is a no-fault state, meaning that drivers are required by law to be covered by personal injury protection (PIP) at a minimum of $10,000. In Florida, each driver must file a claim with their own insurance company before seeking compensation elsewhere.

Clients should note that PIP only covers medical costs and not the costs of property damage. Property damage, including vehicle damages, is covered by property damage liability coverage (PDL). It is also a requirement for every Florida driver to have PDL at a minimum of $10,000. Covering the costs of repairs and replacements of the damaged property can be expensive, so hiring legal representation to help recover these costs can be essential in lessening the financial burdens that usually follow a car accident.

If the damages incurred exceed the maximum policy limit of $10,000, then drivers can file a claim with the insurance provider of the at-fault driver. An experienced Tampa car accident lawyer at The Law Place can help accident victims claim for damages, including medical bills, lost wages, and pain and suffering incurred due to your car accident.

Dealing With Your Insurance Company

When an insurance provider receives a claim after a car accident, the company usually rejects the initial amount put forward by the claimant and looks for flaws in the claim. They do this to dispute the liability of the at-fault party in order to avoid paying out large sums of money to a claimant. For example, an insurance provider may argue that the car repairs made after an accident were not necessary and therefore may refuse to cover the cost of repair to get the car fixed.

By hiring experienced legal representation from The Law Place, you can ensure that you can receive the maximum amount of compensation to cover damages, including the deductible of your insurance provider’s collision coverage. Insurance companies are known for disputing insurance claims made by clients, so having attorneys to fight in your corner is essential. At our law firm, we know how these companies operate, and therefore, we know how to handle them.

What Can a Personal Injury Attorney Do for Me?

First and foremost, a personal injury attorney can explain in detail how car insurance deductibles work and how much of your car insurance deductible you may be able to cover with our help. Our lawyers have ample experience in recovering deductibles that insurance companies impose and can help you to file your claim. As your legal representatives, our team will:

- Determine liability for your accident and decide if your case is strong enough.

- Help claim damages from the at-fault driver’s auto insurance provider if necessary.

- Analyze your car insurance policy and determine your deductible amount.

- Explain the laws and regulations surrounding your legal case.

- Handle negotiations with your insurance provider.

- Gather and record evidence that can strengthen your claim, including photographic evidence of the injuries sustained as well as medical bills and doctor’s records.

- Offer legal advice and consistent communication to keep clients updated on their case.

At The Law Place, we work on a contingency basis as monitored by The State Bar Association. This means you won’t pay any upfront fees for our legal services and will only have to pay a percentage of the total settlement awarded to you if we are successful in your case. We do this as we understand that deductibles can be costly, and covering these costs as well as legal fees and other damages incurred from your accident can cause significant financial challenges.

Resources for Understanding Deductibles in Car Accidents

If you’re involved in a car accident and need guidance on who is responsible for paying the deductible, these resources offer useful information on Florida insurance and accident laws, deductible recovery, and legal assistance:

- The Law Place – Provides a free consultation with attorneys who can help you understand your rights, guide you through the claims process, and advise on deductible recovery options after an accident.

- Florida Department of Highway Safety and Motor Vehicles (FLHSMV) – Offers details on accident reporting requirements, insurance policies, and liability in Florida, including deductible responsibilities in various scenarios.

- Florida Office of Insurance Regulation (OIR) – Explains Florida’s insurance laws, including deductible policies, coverage requirements, and guidelines for filing insurance claims after an accident.

- Florida Statutes – Insurance and Motor Vehicle Laws – Provides comprehensive legal information on Florida’s insurance regulations and motor vehicle statutes, including rules on deductible payments and recovery.

- National Association of Insurance Commissioners (NAIC) – Offers general resources on insurance terms, deductible explanations, and state-specific regulations for managing auto insurance claims.

- Insurance Information Institute (III) – A reliable source of information on car insurance coverage, deductibles, and processes for recovering expenses after an accident, including deductible reimbursement.

These resources can help you understand how deductibles work, who pays them in different accident scenarios, and when you might benefit from legal assistance to secure deductible reimbursement.

Who Pays the Deductible in a Car Accident? FAQ

Does comprehensive coverage require paying a deductible in a motor vehicle accident?

Yes, if you have comprehensive coverage as part of your auto insurance policy, you will typically need to pay a deductible for damages covered by this insurance in a motor vehicle accident. This includes non-collision incidents like theft or weather damage.

Who pays the deductible in a car accident claim?

In a car accident claim, the deductible is generally paid by the policyholder who is filing the claim. Whether this is the at-fault party or not depends on the circumstances of the accident and the specifics of the insurance policies involved.

How does liability insurance affect the need to pay a deductible?

With liability insurance, you generally do not pay a deductible for damages or injuries you cause to others in a car wreck. Liability insurance covers these costs up to your policy limit. However, it does not cover your own damages or injuries.

What happens if my car insurance company disputes my insurance claim?

If your car insurance company disputes your insurance claim, you may need to provide additional evidence to support your claim, negotiate with the company, or seek legal assistance. An experienced car accident attorney can help navigate these disputes.

How does collision insurance work in terms of deductibles?

Collision insurance covers damages to your vehicle from an accident, regardless of who is at fault. When you file a claim under collision insurance, you will typically need to pay a deductible before your insurance carrier covers the remaining costs for repairs.

Is it possible to recover my deductible from the other insurance company in a car accident?

Yes, it is possible to recover your deductible from the other driver’s insurance company if they are found to be at fault. This is typically done through the subrogation process where your insurance company seeks reimbursement from the at-fault party’s insurer.

Will I need to pay out of pocket to get my car repaired if I am not at fault?

If you are not at fault, you may initially have to pay out of pocket for your deductible to get your car repaired. However, you can recover this amount from the at-fault party’s insurance company either directly or through your own insurer’s subrogation process.

How do replacement costs factor into a car accident insurance claim?

Replacement costs factor into a car accident insurance claim if your vehicle is totaled. Your insurance policy may cover the replacement cost of your vehicle, depending on your coverage, minus any deductible you are responsible for.

Contact The Law Place Today

At The Law Place, our attorneys bring together a wealth of experience and a client-centered approach to every case. With a combined experience of over 75 years, our team has successfully handled a range of cases, from personal injury and car accidents to complex criminal defense matters.

Attorneys like David Haenel, a former DUI Prosecutor of the Year, and Stephen C. Higgins, recognized among the Top 100 Trial Lawyers, work collaboratively to provide clients with comprehensive legal support. At The Law Place, we believe in the power of teamwork, and every case benefits from the insights and expertise of our entire legal team, ensuring our clients receive the strongest defense and guidance possible.

Our phone lines are open 24/7, so you can contact us whenever you want. Call us at (941) 444-4444 to schedule your free consultation with a car accident lawyer, who will determine if your deductible can be reimbursed.