When you let someone else drive your car and they get in an accident, your auto insurance typically covers the damages because insurance follows the vehicle, not the driver. This means your insurance policy will be used to cover the costs of the accident, up to your coverage limits. If the damages exceed your policy limits, the driver’s insurance may also come into play.

Attorneys from The Law Place have helped many clients in similar circumstances. As soon as you appoint us, we will assign a skilled Florida personal injury lawyer to your case. If the accident was not the fault of the friend or loved one who was driving your car, your lawyer will be able to seek compensation from the at-fault driver’s insurance provider. You can count on us to help you navigate the entire process effortlessly.

Contact our offices today at (941) 444-4444 to schedule a free consultation, and a lawyer from our team will take you through this situation every step of the way.

Smart Tips for Car Owners Lending Their Vehicle

What are the Consequences of Letting Someone Drive Your Car

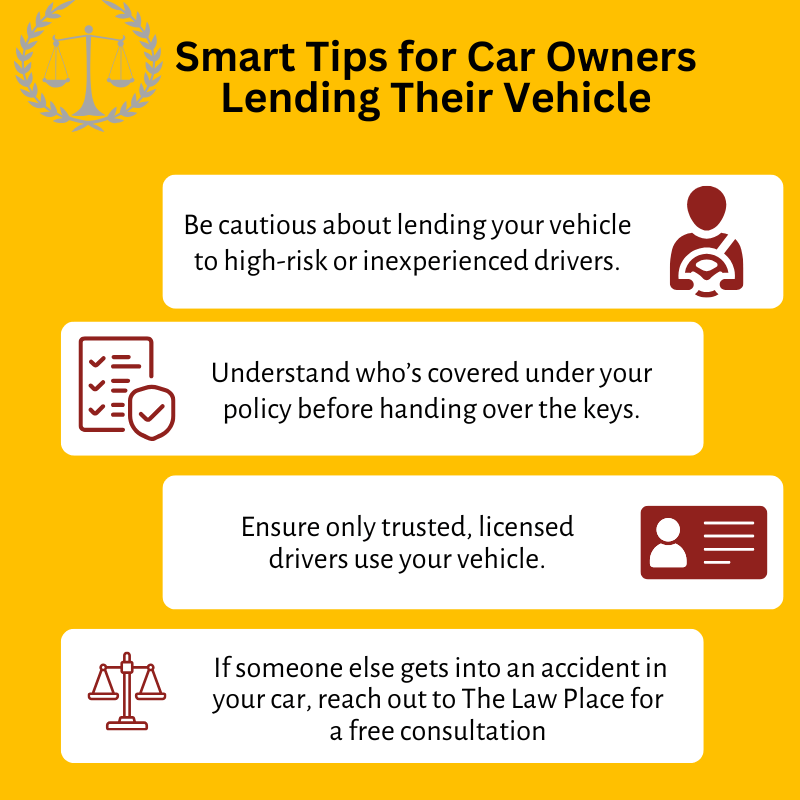

Allowing someone else to drive your car can lead to various legal and financial consequences, especially if they get into an accident. Understanding these implications is crucial when you make the decision to hand over your keys to another driver.

- Insurance Liability – One of the primary concerns is related to insurance coverage. In most cases, your auto insurance policy covers your vehicle, meaning it typically extends to anyone you permit to drive your car. However, if the person driving your car gets into an accident, it is your insurance that will likely bear the primary responsibility for any damages or injuries caused, which could lead to increased premiums in the future.

- Potential for Policy Non-renewal or Cancellation – If the person driving your car causes a significant accident, or if they are an unlicensed or high-risk driver, your insurance provider might consider non-renewal or cancellation of your policy. This is more likely if the accident results in substantial claims that exceed policy limits or if it involves legal complications.

- Legal Responsibility – Depending on the circumstances of the accident, you could also face legal responsibility, especially if you knowingly allowed an impaired, inexperienced, or unlicensed driver to use your vehicle. In such cases, you may be held liable for negligent entrustment, which can lead to lawsuits and potential financial liability for damages and injuries.

- Vehicle Damage and Repair Costs – Any damage to your vehicle in the accident will be your responsibility to repair, especially if the damage exceeds insurance coverage limits or if your policy does not fully cover the type of accident that occurred.

- Possible Criminal Charges – In extreme cases, if the person driving your car commits a criminal act, such as a hit-and-run or driving under the influence, you could potentially face criminal charges, particularly if it’s found that you facilitated or contributed to the criminal behavior.

Permissive and Non-Permissive Use

Depending on whether you gave someone else permission to drive your car, or you didn’t give them permission, this would be called “permissive” or “non-permissive” use. Most large car insurance providers offer permissive use car insurance whilst some smaller companies do not. Again, it is important to review your policy details. Permissive use auto insurance allows occasional use of a vehicle, usually less than 12 times per year, by a driver who does not live at the same address as the policyholder. This could be a relative, a friend, or a neighbor. It would not apply to an immediate family member who lives with you.

- Permissive Use -Permissive use car insurance applies to anyone who has permission to drive your car. If this person gets into an accident, they should get all of the same protections you would get from your car insurance policy. In other words, your car insurance policy should apply to your car and to anyone driving it. Permission can be verbal, and there is no need for it to be written down anywhere.

- Non-Permissive Use – This is when a friend or family member drives your car without your permission. If they get into a car crash, it is unlikely that you will be responsible for third-party damages. However, you may be liable for the damages to your car. In the case of theft, where your vehicle is stolen, and the person driving your car is involved in a collision, you would not be responsible for damages to the other vehicle, but you might have to file a claim with your insurer to cover repairs to your vehicle.

It’s worth noting that unless you explicitly refuse to allow someone else to drive your car, most insurance companies will assume permission was granted. It can be a challenge to prove otherwise.

Two Important Exceptions to Permissive Use Coverage

There are two exceptions to permissive use that you should be aware of:

- Exception one – Permissive use may not cover business uses of your car unless you have included this within your policy. However, if your policy does not cover business uses by permissive users, you will have no coverage if the driver you allowed the use of your car gets into an accident while making a business-related journey.

- Exception two – Permissive use coverage does not apply to unlicensed or inexperienced drivers. If you were not aware that the person you loaned your car to was an unlicensed or inexperienced driver and they got into a car accident, your insurance company might try to deny coverage.

We’re here to serve you. Our phones are open 24 hours a day.

We’re here to serve you. Our phones are open 24 hours a day.

Does Your Car Insurance Cover Other Drivers?

Most people assume that when a friend or family member is driving their car, that person is insured as the driver. However, this is not the case. Insurance applies to the vehicle. So, if someone else is driving your car, and they get into a collision, it will be your insurance that will apply. This is because, in Florida, car insurance follows the vehicle first and the driver second. So, if you allow someone else to drive your car and they get into an accident, your insurance policy will cover that driver and your vehicle, even if they are at fault.

Here is how your insurance policy’s coverage may help:

- Auto Liability Coverage – This may help pay for another person’s medical bills or damaged property linked directly to the accident. Your liability coverage wouldn’t pay for your friend’s medical bills or any repairs to your car.

- Collision Coverage – This may help pay for your vehicle repairs. But, you will be expected to pay your deductible first, which is the amount you agreed to pay before your insurance coverage begins.

- Medical Payments Coverage – This will help if the driver of your vehicle is injured in an accident they caused. This coverage may help pay their medical expenses.

We’re Florida’s top litigation team with over 75 years of combined experience

We’re Florida’s top litigation team with over 75 years of combined experience

The Other Driver’s Insurance

The costs of the car accident might exceed the available coverage on your policy. In this case, the insurance policy of the person who was driving your car may provide additional coverage.

Even if your policy does contain sufficient coverage, your insurance company may still seek reimbursement from the insurance company of the person driving your car. Alternatively, your insurance provider might pay the entire accident claim but will then contact the insurance provider of the person driving your car to claim back some of the costs. All this will depend on the specifics of each party’s insurance policy’s terms and conditions.

From the initial call to updates on your case status, we are here to get you answers.

From the initial call to updates on your case status, we are here to get you answers.

Excluding a Driver

An excluded driver is someone you specifically ask your auto insurance provider not to cover. This could be someone in your family who has a suspended license, a DUI, a poor driving record consisting of numerous speeding tickets, or is simply an inexperienced driver.

If you do not exclude them from your policy, you are likely to see a significant increase in your car insurance costs. By removing them from your car insurance, you agree with your insurer that the excluded driver won’t be allowed to drive your insured vehicle under any conditions.

Excluding them will protect your insurance premium from going up. Once they are removed from your policy documents, your insurance company will update your policy. Then both your insurer and yourself will sign an endorsement to confirm that the named driver will not be covered if they drive your car. However, your policy will still cover them if they are a passenger in your car.

If the excluded driver takes your car without your permission and causes an accident, the insurance company does not have to pay for the damage. Permissive use coverage does not apply here. Both the policyholder and the driver might also be held personally liable for any damages caused to others in the crash.

Who Are Named Drivers?

This will tend to be drivers within your family household who are specifically named in your car insurance policy. Most insurers will ask you to list these individuals when you apply for car insurance, as well as any other people that regularly use your car.

The definition of a “household member” within insurance policies is usually someone that is living in your home and is related to you by blood, marriage, or adoption. If you have a roommate or housemate who would like to be covered by your car insurance, then you should check to see if that person can be covered as a household member. If the answer is no, then you should list them as a named driver instead. Failure to inform your insurance company about someone who you know will drive your car is a misrepresentation, a form of insurance fraud.

Giving Permission to an Uninsured or Unlicensed Driver Is a Crime

In Florida, allowing an unlicensed driver permission to drive your vehicle is considered a criminal offense. You could face fines up to $500 or even up to two months of incarceration.

Florida Statute 322.36 states that a person cannot authorize or knowingly permit a motor vehicle owned by themselves to be operated on any highway or public street by a person who is not lawfully licensed to drive.

This means that if you are going to allow an uninsured or unlicensed person to drive your vehicle, or you allow this person to drive your vehicle while you are a passenger, then you could be charged with a second-degree misdemeanor.

Penalties for Permitting an Unauthorized Driver

Under Florida law, second-degree misdemeanors are punishable by:

- Up to 2 months in prison.

- Up to 6 months of probation.

- Up to $500 in fines.

You must be careful when handing your car keys over to someone else. If the driver causes a car accident in your vehicle, then you could be arrested for allowing them to drive. There are several potential defenses to this charge, such as in the case of an emergency or necessity. Your lawyer will be able to advise you on this.

Things to Keep in Mind

- Be mindful about who drives your car.

- If you feel uncertain about the ability of someone to safely operate your vehicle, don’t let them use it.

- Don’t make your keys easily accessible if you know that someone will be tempted to drive your car – such as an inexperienced young driver.

- Understand the terms and conditions within your insurance policy for lending out your car to other drivers.

- If someone uses your vehicle more than 12 times a year, consider adding them as an additional named driver under your insurance policy.

- Exclude drivers with a bad driving record and protect your own insurance premium from going up.

- Make sure that if you do lend out your car, it’s to someone with a valid driver’s license and that you trust them with your car.

- Say no, and stick to it, when someone with a poor driving record asks to borrow your car.

- Make sure your insurance information and vehicle registration are in your glove box.

- Consider adding bodily injury liability (BIL) coverage to your insurance policy.

Resources for Understanding Liability When Someone Else Drives Your Car

If someone else was driving your car and got into an accident, these resources can help clarify insurance responsibilities, liability, and next steps for managing claims and coverage:

- The Law Place – Offers a free consultation with experienced attorneys who can help you understand your rights and liabilities if someone else crashes your car. They can also guide you on how to navigate claims with insurance companies.

- Florida Department of Highway Safety and Motor Vehicles (FLHSMV) – Provides information on Florida’s insurance and liability laws, including guidelines on accidents involving drivers who are not the vehicle owner.

- Florida Office of Insurance Regulation (OIR) – Details Florida’s insurance requirements and offers explanations of coverage types, liability policies, and regulations on claims when someone else is at fault while driving your vehicle.

- Insurance Information Institute (III) – Offers explanations of various insurance coverage scenarios, including liability when someone else drives your car and has an accident, as well as insights on claim handling and insurance responsibilities.

- National Association of Insurance Commissioners (NAIC) – Provides information on how different states handle insurance and liability when a non-owner driver is involved in an accident, along with guidelines for managing the claims process.

These resources can help you navigate the responsibilities and liabilities involved when someone else is driving your vehicle, assisting you in understanding Florida’s specific laws and insurance requirements.

What Happens When You Let Someone Else Drive Your Car and They Get in an Accident? FAQ

What happens if someone else drives my car and gets in an accident, who pays for the damages?

When someone else drives your car and gets in an accident, your liability insurance typically covers damages up to your policy limits. Auto insurance usually follows the car rather than the driver, so your own auto insurance policy is considered the primary coverage for damages or injuries caused by the accident. However, if the damages exceed your policy limits, the driver’s own insurance might come into play as secondary coverage.

Does my car insurance cover injuries to the other driver or pedestrians if my friend was at fault?

Yes, if your friend was the at fault driver, your car insurance coverage generally includes liability insurance for bodily injuries and property damage up to your policy limits. This means your policy may cover injuries to others involved in the accident, such as the other driver or pedestrians, depending on your coverage specifics. If injuries or damages are significant, you may want to consult a personal injury lawyer for further guidance.

Will letting my friend drive my car affect my insurance rates?

Yes, it’s possible. If an insurance claim is filed due to an accident caused while someone else was driving, your auto insurance company may increase your premium, even though you weren’t the one driving. Premium changes vary by insurer and the specifics of the accident, so contact your insurance agent for a clearer picture.

Can my friend’s insurance company cover the accident instead?

Not usually. Since your insurance is the primary coverage, it’s responsible for the damages first. However, if the accident costs exceed your policy limits, your friend’s insurance company may cover the excess amount. This is called secondary coverage.

What if the accident causes extensive injuries or fatalities?

If severe injuries or fatalities are involved, your liability limits may not be enough to cover the damages. In such situations, it may be wise to consult a personal injury lawyer who can help navigate the complexities of coverage, liability, and possible litigation.

Contact The Law Place Today

If someone else drives your car and gets into an accident, then you should act quickly. Please pick up the phone and speak to one of our legal representatives now. The Law Place has a highly trained team of car accident lawyers with over 75 years of experience. We have the confidence and skill to take on complex and challenging cases.

The moment you appoint us, we’ll start preparing your case. Insurance companies are notorious for finding ways to pay out less than the accident costs are worth. We promise to make sure that your rights are protected and that you get the compensation you deserve.

Our team of car accident lawyers is here to give you the legal advice that you need, and we have the knowledge to do exactly that. Our law firm will make sure that the whole process is as straightforward as possible for you.

You can contact us on (941) 444-4444, and a Sarasota personal injury lawyer will assist you in getting any compensation you are entitled to. Our phone lines are open twenty-four hours a day, seven days a week. Set up a free consultation today!